.png)

Retail: A growth engine for the Indian economy

Dear Patron,

The retail industry is one of the largest and the fastest growing sector in Indian economy, with >10% contribution to GDP (Refer Exhibit: 1&2). Buoyed by rising income levels, consumerism and rapid urbanisation, retail has been a crucial part of India’s growth story. BCG expects it to reach $2 tn by 2032 growing by ~9-10% CAGR. This is expected to fundamentally alter the consumption basket over the coming decade. In this newsletter, we will understand the evolution of retail sector in India, future growth levers and the impact it has had on our portfolio companies.

Exhibit 1: Retail contribution to GDP is expected to rise considerably

Source: Ambit Asset Management, IBEG.ORG

Exhibit 2: India's retail industry has significant headroom for growth when compared with global benchmarks

|

India |

USA |

UK |

|

|

Size of Retail Market ($trn) in 2021 |

0.7 |

3.8 |

0.6 |

|

Historical Growth (CAGR 2010-2019) |

>10% |

3-4% |

0-1% |

|

Expected Growth for the next decade |

9-10% |

Global Retail Sector growth - 3%-4% |

|

Exhibit 3 - Retail Market in India expected to grow by ~9-10% CAGR from 2020-2030E

Source: Statista.com, Ambit Asset Management

Evolution of Retail in India:

Over the years, Retail as a sector in India, has been one of the most dynamic and fast paced industries, having gone through several phases:

- Pre 1990s (traditional retail): Traditional stores characterised by individual sellers offering variety of goods under one roof. Eg. Mom & Pop stores

- 1990-2000 (emergence of organised retail): With liberalization in the 1990s, pure play retailers realised the potential of this industry. Indian cities saw the rise of departmental stores, retail chains and shopping malls. Example: Mr Kishore biyani, founder of Pantaloons’ retail who pioneered modern retail in India, had opened first Pantaloons store in 1997

- 2000-2010 (modern retail expansion): In this phase, growth of modern retail accelerated. Domestic big players like Big Bazaar, Dmart entered the market offering a wide range of products under one roof.

- 2010-2020 (e-commerce boom): The advent of the internet and the rise in e-commerce brought a significant transformation in retail. Companies like flipkart, amazon, snapdeal emerged as popular online shopping destinations.

- Post Covid (shift towards omni channel retail): With the increase in penetration of smartphones and internet connectivity. retailers started adopting omni channel approach. They integrate online and offline channel to provide seamless shopping experience.

Key levers for a $2trn Retail industry by 2032

1. Rise in disposable income leads to increase in discretionary spend:

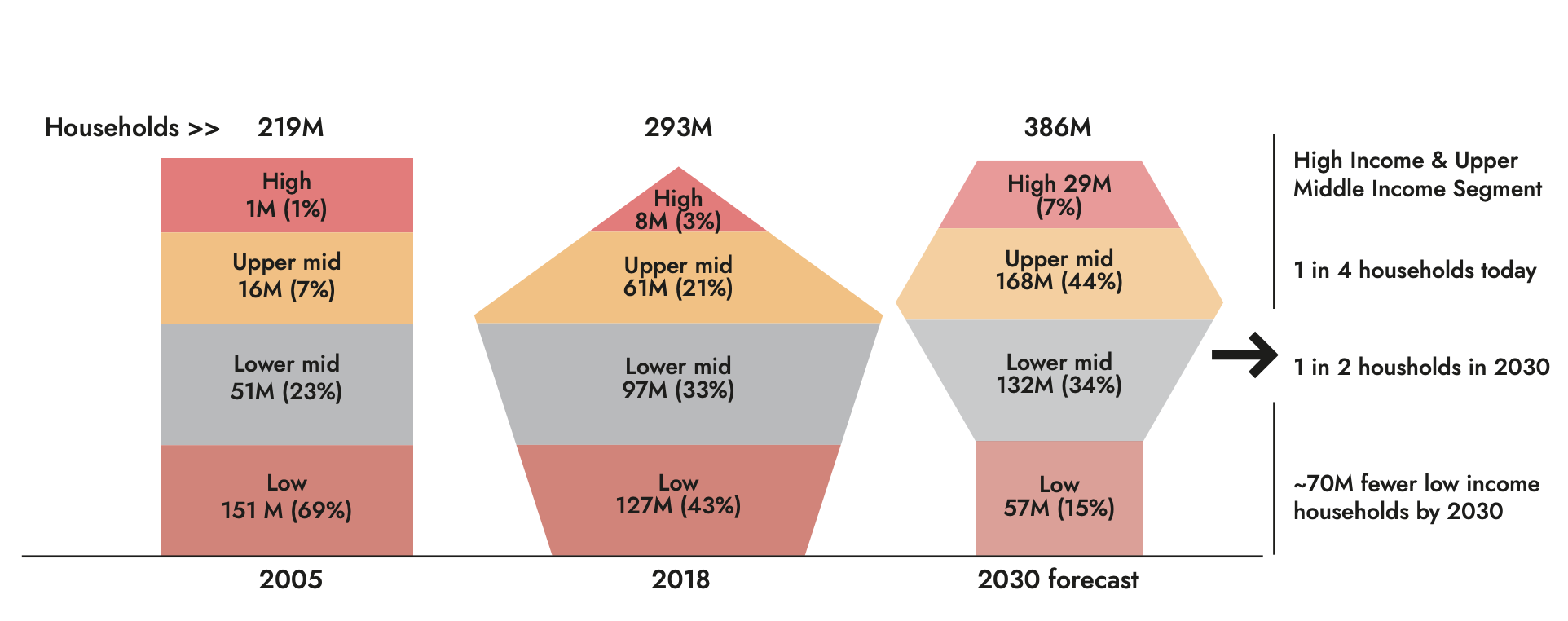

With growing GDP per capita (~9% CAGR over FY15-FY23), rise in income levels, rapid urbanization and exposure to global trends, Indian consumers are aspiring for a higher standard of living. Growth in income levels will transform the lifestyle of bottom of the pyramid population in addition to higher spend by mid-income consumers propelling consumer spend to ~$6tn by 2023.

Exhibit 4: Growth in income will transform discretionary consumer spending over next decade

Source: WEF, Bain report, Ambit Asset Management

2. Burgeoning millennial population & evolving consumer attitude:

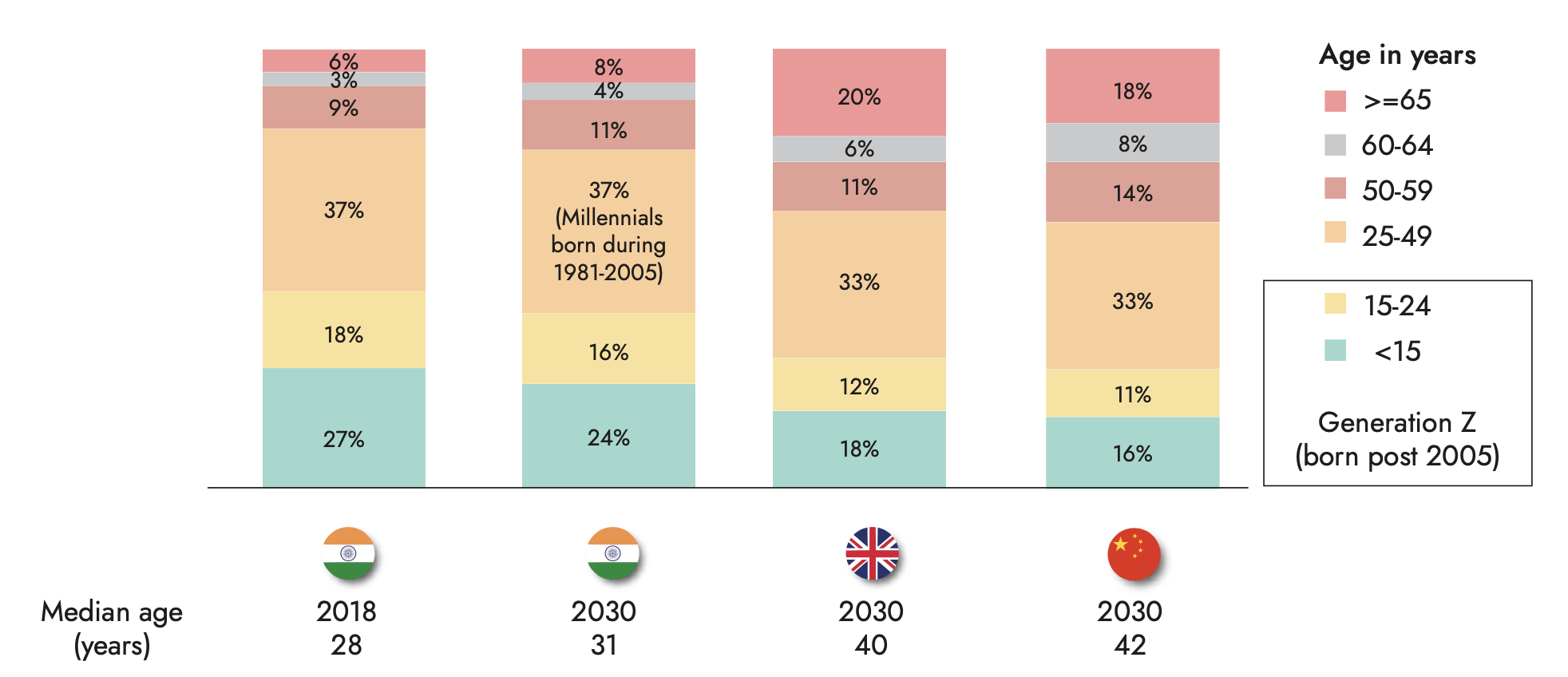

India will remain a nation of the young with one of the largest working-age population (Median age 31 years) by 2030, (Refer Exhibit 5) unlike many ageing nations in the West (40 years) and East (42 years). India will likely see the transformation over the next decade in household consumption patterns as the current generation breaks away from the frugal and save-first lifestyle of their preceding generations, and are happy to spend money on quality, convenience and an improving lifestyle.

Exhibit 5: Favorable demographics with working age majority will drive future consumption growth in India

Source: Euro monitor, Ambit Asset Management

3. Govt initiative & policy support creates better investment opportunities:

The Indian government's liberalization of FDI policies in the retail sector has attracted significant investment from domestic and international players (Refer Exhibit 6). This has led to increased participation by global investors in the sector either via strategic investments or greenfield projects.

Exhibit 6: Retail Industry high growth potential is attracting foreign investments

|

Type |

Company |

Investment in India |

|

Foreign Investments |

IKEA - the Swedish furniture maker |

Rs 8.5bn over next few years |

|

Foreign Investments |

Lulu Group - a UAE-based retail company |

Rs 20bn to develop shopping malls. |

|

Foreign Investments |

H&M - Swedish retailer |

Rs 7.2bn |

|

Acquisition |

Reliance Retail |

acquired Just Dial |

Source: Company website, AR, Ambit Asset Management

4. Revolutionizing access to Finance and ease of consumer credit

Easing consumer credit access courtesy the tie-ups between Banks/NBFC and retailers & the rise of emerging payment modes such as ‘Buy Now, Pay Later’ (BNPL) have enabled consumers to spend more easily on high ticket discretionary spends.

Example: Bajaj Finance pioneered the easy consumer credit access. This was followed by various new initiatives such as Credit Card EMI purchase, BNPL, etc. which have all enabled consumers to spend more on discretionary purchases.

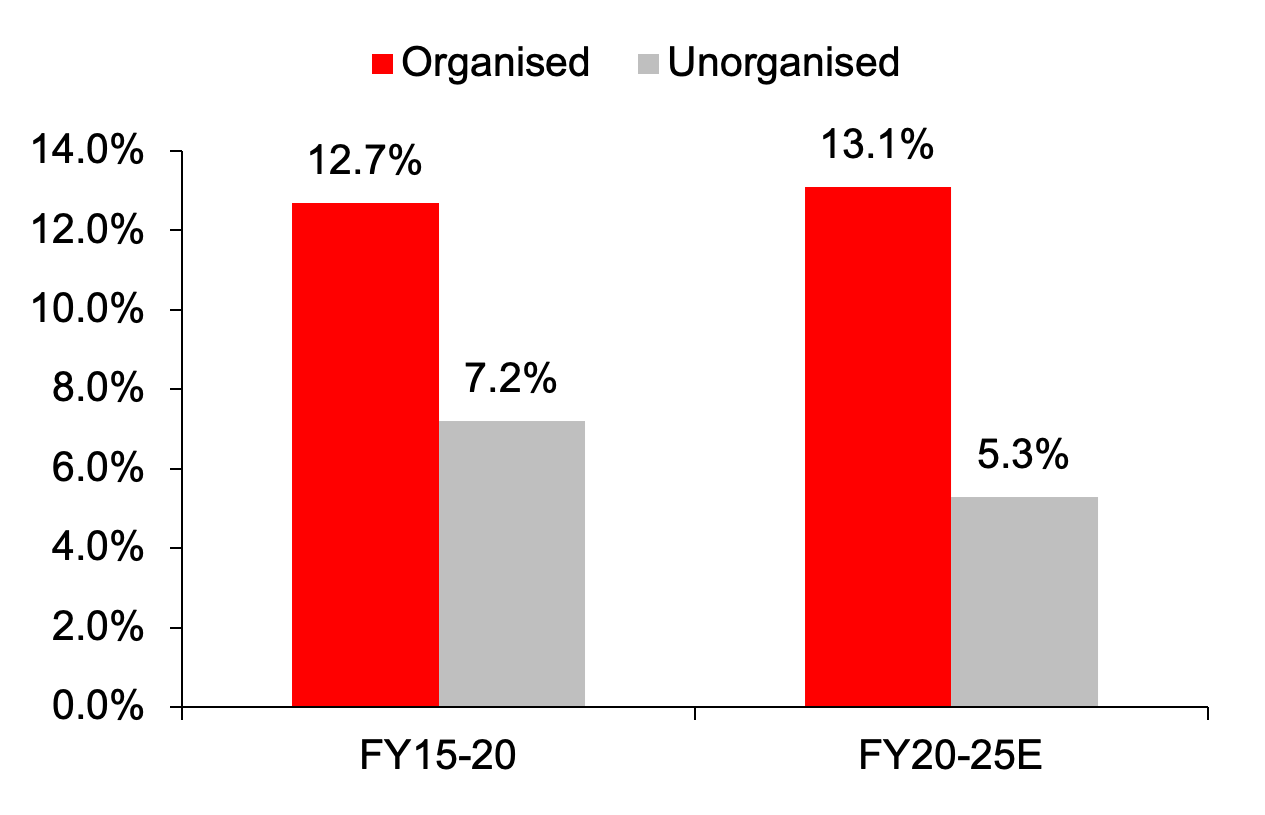

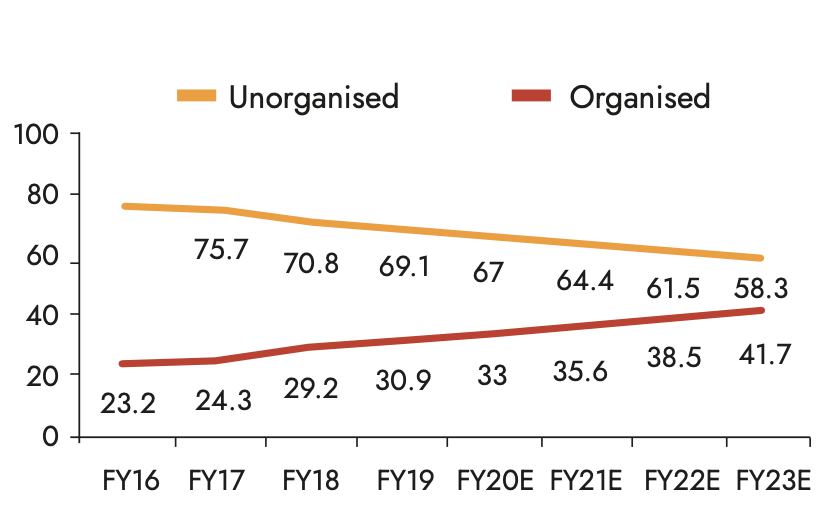

5. High growth trajectory of organized retail industry:

The India retail industry is at an inflection point where the share of organized retail is expanding at an exponential rate, following government reforms such as increase in FDI limit, demonetization & GST. The organized retail industry is expected to grow at ~11% CAGR over 2023-2032 led by major developments in Tier 2/3 cities

The proliferation of e-commerce and digital technologies alongside covid limitations has acted as a catalyst for the growth of organized retail. The rapid evolution of omni-channel and digital adoption combined with infrastructure developments has a huge potential for future growth in the organized retail industry.

Exhibit 7: The E-commerce sector in India has been experiencing exponential growth

Souce: BCG-RAI report, Ambit Asset Management

The major investment themes to play with the big cheer in Indian Retail sector with relevant examples from our portfolios:

1. Shift towards unorganized to organized

Safari Industries, which primarily operates in the value segment, has benefitted the most due to its strong price positioning. During covid, luggage industry was teetering on the brink of collapse due to a) weak demand because of travel and tourism slowdown and b) high cost of operations owing to disruption in supply change from China. This had added to the woes of the unorganized players dependent on China. Safari tackled the issue well by diversifying operations from China to India & Bangladesh. As a result, Price differential between unbranded (largely dependent on Chinese imports) and mass branded declined from 50% to 20%. This led to most of the first-time travelers preferring branded luggage over unbranded luggage.

Exhibit 8: Safari Industries rightly positioned to cater to shift in demand from unorganized segment. Leading to market share gains

Source: Company website, Ambit Asset management

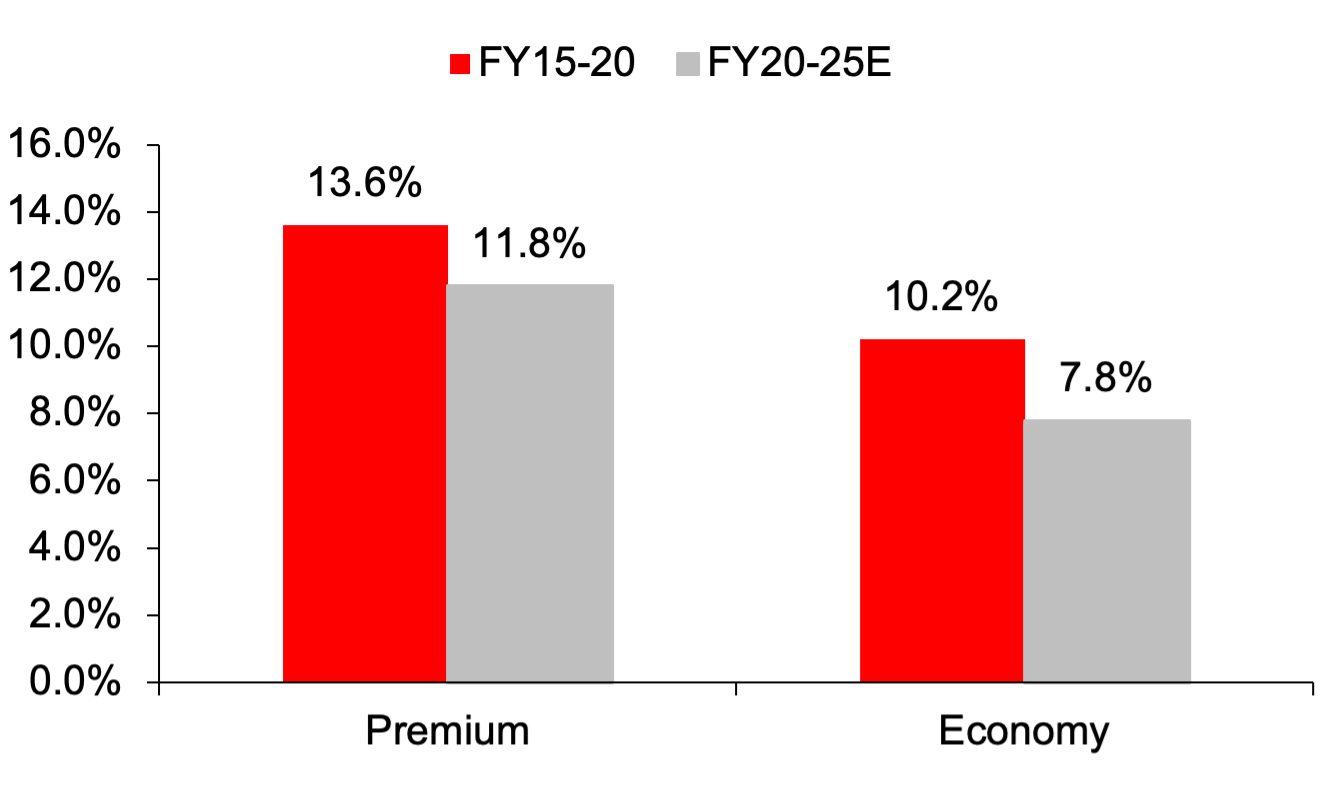

2. Premiumization play owing to rise in aspirational consumers:

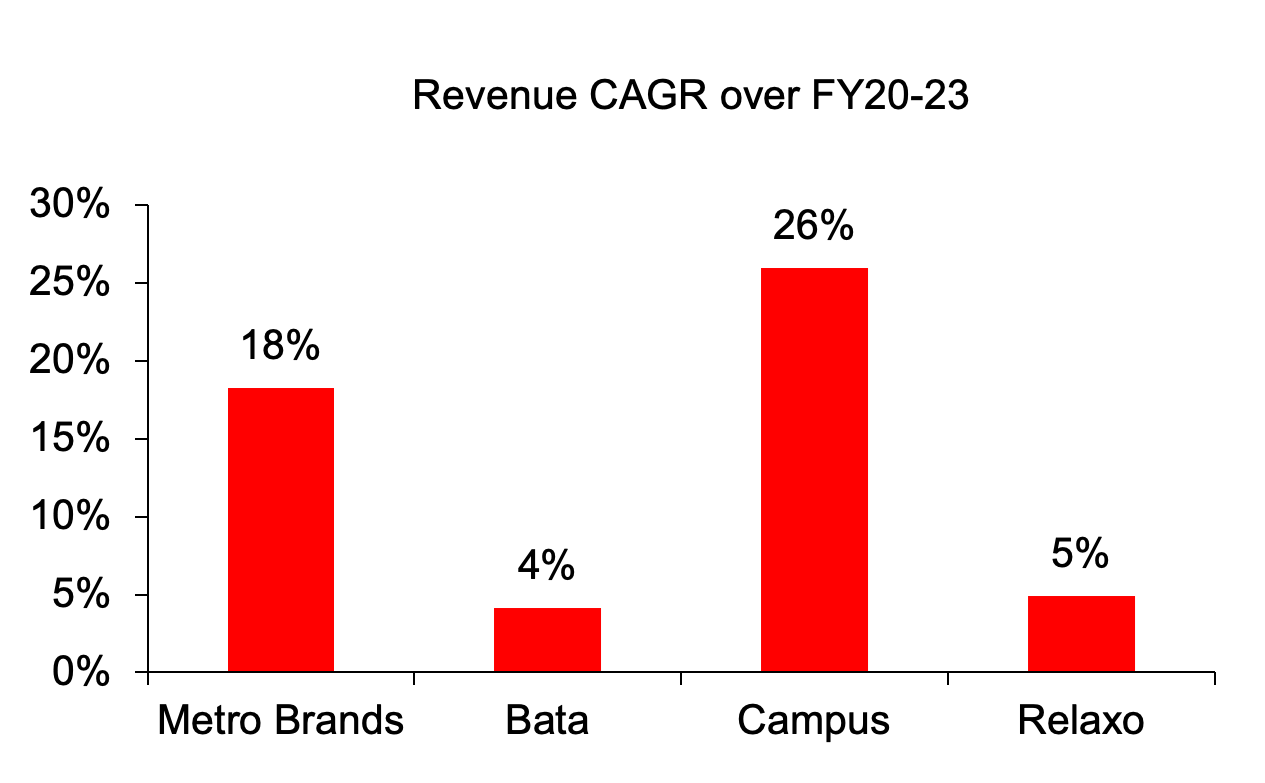

Metro Brands targets the mid - to premium segment (Refer Exhibit xx) of the footwear market catering to a price-conscious but aspirational consumer segment. Metro’s strategy to operate in multiple formats viz. Metro, Mochi & Crocs enabled it to cater to a wide range of consumers and garner higher share in the organized mid to premium segment. Metro was a key beneficiary of the earlier talked about premiumization / higher aspiration trend of Indian youth in the entire listed footwear space.

Exhibit 9: Higher growth in organized segment led by Increase in aspirational consumers and Premiumization play benefitted the Co.

Source: Campus, RHP, Ambit Asset Management

Exhibit 10: Metro Brands premium positioning drives higher revenue growth vs other mass players

Source: Companies’ investor presentation, Ambit Asset Management

3. Rapid Urbanization:

India’s leading apparel retailer Trent Ltd. has started aggressive store expansion post covid by opening larger stores across its format in tier 2/3 cities as against industry trend of opening small stores in tier2/3 cities. In case of its flagship formats, it has added over 300 stores during FY 2020-23 which has given 33% revenue CAGR as against apparel industry CAGR of 15%

Exhibit 11: Trent's rapid store expansion strategy accelerated revenue growth

Source: Trent's AR, Ambit Asset Management

4. "Omni" channel strategy:

Titan Company Ltd. fully utilized the limitation of pandemic as an opportunity to expand its store network, adopt aggressively. Omni channel strategy alongside regulatory tailwind such as compulsory hallmarking and demonetization helped consolidate market share from unorganized segment.

Exhibit 12: Jewelry Organized Market consistently expanding... Leading to robust revenue growth for Titan Company Ltd.

Source: Titan Company Ltd., Investor Presentation, Ambit Asset Management

CONCLUSION:

India’s retail sector will be a key driver of $10tn GDP over the next 10-13 years. It has bounced back strongly after COVID blues to cross pre-COVID levels. The industry is expected to reach $2tn by 2032 implying a CAGR of 9-10%. Currently, Retail in India is growing at a strong clip and creating new opportunities for retailers. However, the changing landscape demands retailers to be receptive to change and more agile in response to shifting consumer preferences. The next decade will see organised retailers focus more on footprint expansion across all formats - offline and online - to fuel future growth.

Companies in our portfolio like Titan, Trent, Go Fashion, Metro brands etc. are best positioned to benefit out of this tailwind. They have been nimble footed in transitioning to Omni channel platforms, expanding in tier2/3 cities and creating better brand awareness and deeper emotional connect with consumers.

Ambit Coffee Can Portfolio

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has an unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced with disruptions at regular intervals. As the industry evolves or is faced with disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

Exhibit 13: Ambit’s Coffee Can Portfolio point-to-point performance

Source: Ambit Asset Management; Portfolio inception date is March 6, 2017; Returns as of June 30th 2023; All returns are post fees and expenses; Returns above 1 year are annualized; Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts. * Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio and the same is reported to SEBI.

Exhibit 14: Ambit’s Coffee Can Portfolio calendar year performance

Source: Ambit Asset Management; Portfolio inception date is March 6, 2017; Returns as of June 30th 2023; All returns are post fees and expenses. Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts. * Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio and the same is reported to SEBI.

Ambit Good & Clean Midcap Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver superior risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

- Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

- Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longer with annual churn not exceeding 15-20% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with these compounding earnings acting as the primary driver of investment returns over long periods.

- Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

Exhibit 15: Ambit’s Good & Clean Midcap Portfolio point-to-point performance

Source: Ambit Asset Management; Portfolio inception date is March 12, 2015; Returns as of June 30th 2023; All returns above 1 year are annualized. Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Midcap strategy and the same is reported to SEBI. In addition to the same, we have included the Nifty Midcap 100 and MF Peers for information purposes only. The same should not be relied upon for performance benchmarking in any manner. MF Peers: HDFC MF, Kotak MF, SBI MF, Franklin India MF, Aditya Birla Sunlife MF, Axis MF, L&T MF, MOSL MF, ICICI Prudential MF

Exhibit 16: Ambit’s Good & Clean Midcap Portfolio calendar year performance

Source: Ambit Asset Management; Portfolio inception date is March 12, 2015; Returns as of June 30th 2023. Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Midcap strategy and the same is reported to SEBI.

Ambit Emerging Giants Portfolio

Small caps with secular growth, superior return ratios and no leverage – Ambit's Emerging Giants portfolio aims to invest in small-cap companies with market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than Rs4,000cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt), and the ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence lead us to a concentrated portfolio of 15-16 emerging giants.

Exhibit 17: Ambit Emerging Giants Portfolio point-to-point performance

Source: Ambit Asset Management; Portfolio inception date is December 1, 2017; Returns as of June 30th 2023; All returns above 1 year are annualized. Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants strategy and the same is reported to SEBI.

Exhibit 18: Ambit Emerging Giants Portfolio calendar year performance

Source: Ambit Asset Management; Portfolio inception date is December 1, 2017; Returns as of June 30th 2023 Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants strategy and the same is reported to SEBI.

Ambit TenX Portfolio

Ambit TenX Portfolio gives investors an opportunity to participate in the India growth story as the Indian GDP heads towards a US$10tn mark over the next 12-15 years. Mid and Small corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that can grow their earnings 10x over the same period implying 18-21% CAGR.

Key features of this portfolio would be as follow:

- Longer-term approach with a concentrated portfolio: Ideal investment duration of >5 years with 15-20 stocks.

- Key driving factors: Low penetration, strong leadership, light balance sheet

- Forward-looking approach: Relying less on historical performance and more on future potential while not deviating away from the Good & Clean philosophy. No Key-man risk: Process is the Fund Manager

Exhibit 19: Ambit TenX Portfolio point-to-point performance

Source: Ambit Asset Management; Portfolio inception date is December 13, 2021; Returns as of June 30th 2023; Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio and the same is reported to SEBI.

Exhibit 20: Ambit TenX Portfolio calendar year performance

Source: Ambit Asset Management; Portfolio inception date is December 13, 2021; Returns as of June 30th 2023. Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio and the same is reported to SEBI.

For any queries, please contact:

Umang Shah- Phone: +91 22 6623 3281, Email - [email protected]. Ambit Investment Advisors Private Limited - Ambit Investment Advisors Private Limited 2103/2104, 21st Floor, One Lodha Place, Senapati Bapat Marg,

Lower Parel, Mumbai - 400 013

Risk Disclosure & Disclaimer

The performance of the Portfolio Manager has not been approved or recommended by SEBI nor SEBI certifies the accuracy or adequacy of the performance related information contained therein.

Ambit Investment Advisors Private Limited (“Ambit”), is a registered Portfolio Manager with Securities and Exchange Board of India vide registration number INP000005059.

This presentation / newsletter / report is strictly for information and illustrative purposes only and should not be considered to be an offer, or solicitation of an offer, to buy or sell any securities or to enter into any Portfolio Management agreements. This presentation / newsletter / report is prepared by Ambit strictly for the specified audience and is not intended for distribution to public and is not to be disseminated or circulated to any other party outside of the intended purpose. This presentation / newsletter / report may contain confidential or proprietary information and no part of this presentation / newsletter / report may be reproduced in any form without its prior written consent to Ambit. All opinions, figures, charts/graphs, estimates and data included in this presentation / newsletter / report is subject to change without notice. This document is not for public distribution and if you receive a copy of this presentation / newsletter / report and you are not the intended recipient, you should destroy this immediately. Any dissemination, copying or circulation of this communication in any form is strictly prohibited. This material should not be circulated in countries where restrictions exist on soliciting business from potential clients residing in such countries. Recipients of this material should inform themselves about and observe any such restrictions. Recipients shall be solely liable for any liability incurred by them in this regard and will indemnify Ambit for any liability it may incur in this respect.

Neither Ambit nor any of their respective affiliates or representatives make any express or implied representation or warranty as to the adequacy or accuracy of the statistical data or factual statement concerning India or its economy or make any representation as to the accuracy, completeness, reasonableness or sufficiency of any of the information contained in the presentation / newsletter / report herein, or in the case of projections, as to their attainability or the accuracy or completeness of the assumptions from which they are derived, and it is expected each prospective investor will pursue its own independent due diligence. In preparing this presentation / newsletter / report, Ambit has relied upon and assumed, without independent verification, the accuracy and completeness of information available from public sources. Accordingly, neither Ambit nor any of its affiliates, shareholders, directors, employees, agents or advisors shall be liable for any loss or damage (direct or indirect) suffered as a result of reliance upon any statements contained in, or any omission from this presentation / newsletter / report and any such liability is expressly disclaimed. Further, the information contained in this presentation / newsletter / report has not been verified by SEBI. You are expected to take into consideration all the risk factors including financial conditions, risk-return profile, tax consequences, etc. You understand that the past performance or name of the portfolio or any similar product do not in any manner indicate surety of performance of such product or portfolio in future. You further understand that all such products are subject to various market risks, settlement risks, economical risks, political risks, business risks, and financial risks etc. and there is no assurance or guarantee that the objectives of any of the strategies of such product or portfolio will be achieved. You are expected to thoroughly go through the terms of the arrangements / agreements and understand in detail the risk-return profile of any security or product of Ambit or any other service provider before making any investment. You should also take professional / legal /tax advice before making any decision of investing or disinvesting. The investment relating to any products of Ambit may not be suited to all categories of investors. Ambit or Ambit associates may have financial or other business interests that may adversely affect the objectivity of the views contained in this presentation / newsletter / report.

Ambit does not guarantee the future performance or any level of performance relating to any products of Ambit or any other third party service provider. Investment in any product including mutual fund or in the product of third party service provider does not provide any assurance or guarantee that the objectives of the product are specifically achieved. Ambit shall not be liable for any losses that you may suffer on account of any investment or disinvestment decision based on the communication or information or recommendation received from Ambit on any product. Further Ambit shall not be liable for any loss which may have arisen by wrong or misleading instructions given by you whether orally or in writing. The name of the product does not in any manner indicate their prospects or return.

The product ‘Ambit Coffee Can Portfolio’ has been migrated from Ambit Capital Private Limited to Ambit Investments Advisors Private Limited. Hence some of the information in this presentation may belong to the period when this product was managed by Ambit Capital Private Limited. You may contact your Relationship Manager for any queries.

The performance data for coffee can product between 6th march 2017 - 19th June 2017 represents model portfolio returns. First client was onboarded on 20th June 2017. The performance data for G&C product between 1st June 2016 to 1st April 2018 also includes returns for funds managed for an advisory offshore client. Returns are calculated using TWRR method as prescribed under revised SEBI (Portfolio Managers) Regulations, 2020